If you are considering a mortgage in the UK, a fixed mortgage could provide stability and predictable repayments. It offers predictable payments, helping homeowners and first-time buyers plan their finances more easily. But what exactly is a fixed mortgage, and how does it work? Let’s dive into the details.

What is a Fixed Mortgage?

A fixed mortgage is a type of home loan where the interest rate remains the same for a specified period, ensuring stable monthly payments. This means your mortgage payments won’t fluctuate even if interest rates in the market rise. For example, if you secure a 5-year fixed mortgage, your monthly payment stays the same for the entire five years, offering a sense of financial security.

The History and Evolution of Fixed Mortgages in the UK

Fixed mortgages have been a cornerstone of home financing in the UK for many decades. Initially, mortgages with variable interest rates dominated the market, leaving homeowners vulnerable to fluctuations in interest rates. In the 1980s, however, fixed-rate mortgages began to gain popularity as a means of providing more financial predictability for homeowners.

The 1990s saw a rise in the availability of longer-term fixed-rate deals. During periods of economic instability, especially when the Bank of England raised interest rates to control inflation, homeowners began to see the benefits of locking in a fixed rate. Over the years, lenders have introduced a variety of fixed-rate mortgage options, making them more flexible and accessible to first-time buyers, as well as homeowners looking to remortgage.

As the UK housing market evolved, mortgage products tailored to various borrower needs emerged, such as the option for buy-to-let investors to secure fixed-rate deals. Today, fixed mortgages are considered one of the most reliable and secure types of mortgages for people who value stability in their payments.

How Fixed Mortgages Work

With a fixed mortgage, you agree to a certain interest rate for a specific term. This could range from two to ten years, with some lenders offering longer periods. For the duration of this term, your interest rate will remain unchanged. This means your monthly payments are predictable, and you won’t be affected by fluctuations in the Bank of England base rate or other market factors.

One of the key features of a fixed mortgage is that it helps you plan your finances without worrying about unexpected spikes in your mortgage payments. Whether you’re a first-time buyer or remortgaging, the stability that comes with a fixed mortgage can make it easier to budget over the long term.

Benefits of a Fixed Mortgage

Same Payment Every Month

A major advantage of a fixed mortgage is the ability to plan your finances more easily. Because your payments are the same each month, you won’t have to worry about fluctuating mortgage rates eating into your monthly budget.

Easy to Plan Your Future

A fixed mortgage gives you confidence in your financial planning. Knowing exactly how much you’ll pay each month allows you to better manage your spending and savings goals.

Protection from Rate Increases

One of the most significant advantages of a fixed mortgage is that it shields you from interest rate hikes. If market rates increase during your fixed term, your mortgage payments will remain unchanged.

Less Stress and More Peace of Mind

The predictability of fixed payments provides peace of mind. You won’t be caught off guard by an unexpected rate rise, which can often lead to financial stress.

Simple and Beginner-Friendly

For first-time buyers, fixed mortgages are an easy-to-understand option. With no surprise interest rate changes, you know exactly what to expect each month.

Types of Fixed Mortgages in the UK

There are different types of fixed mortgages available, depending on how long you want to lock in your interest rate.

2-Year Fixed

A two-year fixed mortgage typically comes with a lower interest rate, but it offers less long-term stability. After the two years, your mortgage will revert to the lender’s standard variable rate, which could be higher.

3-Year Fixed

The three-year fixed mortgage is ideal for homeowners who want to lock in a predictable rate for a bit longer. It provides more stability than the two-year option but still allows for flexibility after the fixed term.

5-Year Fixed

The five-year fixed rate mortgage is one of the most common options for borrowers. It offers a balance of stability and affordability, ensuring consistent payments for a reasonable length of time.

10-Year Fixed

A ten-year fixed mortgage locks in your rate for an entire decade. This type of mortgage is perfect for those who want maximum stability and are committed to staying in their home for the long term.

How to Choose the Right Fixed Mortgage for You

Choosing the right fixed mortgage requires careful consideration of your financial goals and circumstances.

Decide How Long to Fix For

The first step is deciding how long you want to fix your mortgage. If you plan on staying in your home for a while, a longer term might be a better option. However, if you think you may move soon, a shorter fixed term might be more suitable.

Check if You Want Stability or Flexibility

Consider whether you prefer the stability of fixed payments or the flexibility of a variable mortgage. A fixed mortgage offers more security, while a variable mortgage could provide lower payments if interest rates fall.

Look at the Whole Cost, Not Just the Rate

It’s important to compare the overall cost of the mortgage, not just the interest rate. Consider fees, penalties for early repayment, and any additional charges.

Make Sure the Payment Fits Your Budget

Before committing, ensure that the monthly payment fits comfortably within your budget. You don’t want to stretch your finances too thin by taking on a mortgage that you can’t afford in the long run.

Think About How Long You Will Stay in the Home

If you plan to stay in the house for a long time, a long-term fixed mortgage might be the best choice. However, if you think you’ll move before your fixed term ends, consider a shorter-term mortgage.

Check Your Credit and Deposit

Lenders will check your credit score and deposit amount before offering you a fixed mortgage deal. Make sure your credit score is in good shape and that you can afford the required deposit.

Compare Offers and Get Advice if Needed

Don’t settle for the first offer you see. Shop around and compare fixed mortgage deals from different lenders. If needed, consult a mortgage advisor to help you make the best decision.

Pros and Cons of Fixed Mortgages

When considering a fixed mortgage, it’s essential to weigh both its advantages and disadvantages. While fixed mortgages offer stability, there are a few factors to keep in mind before committing. Let’s break down the pros and cons in more detail:

Pros:

Easy to Plan Your Budget

One of the main benefits of a fixed mortgage is that it makes budgeting straightforward. With a fixed rate, your monthly payments remain the same throughout the entire term of your mortgage. This predictability allows you to plan your finances with confidence, knowing exactly how much you need to pay every month.

Protection if Rates Go Up

A fixed mortgage protects you from rising interest rates. Even if market rates increase, your mortgage payment stays the same. This is especially helpful when interest rates are expected to rise, as you won’t be affected by those increases. It offers peace of mind, knowing your payments will remain consistent, regardless of external market factors.

Simple and Easy to Understand

For first-time buyers, fixed mortgages are relatively easy to understand. There are no surprises with fluctuating payments or complex calculations. It’s simply a straightforward loan with an interest rate that won’t change, making it one of the most accessible mortgage options for new homeowners.

Cons:

Often Higher Starting Rate

Fixed mortgages often come with a higher starting interest rate compared to variable mortgages. This means you may pay more upfront, especially if market rates are lower when you sign the contract. The higher initial rate can make fixed mortgages less appealing for those who are looking for the lowest possible monthly payment.

Not Flexible If Rates Fall

If interest rates fall after you’ve locked in a fixed rate, you won’t benefit from the lower rates unless you refinance. This lack of flexibility is a downside for those who want to take advantage of lower interest rates in the future. It can be frustrating if the market rate drops, but you’re stuck with your fixed rate.

Long Commitment

Choosing a fixed mortgage usually means committing to a set interest rate for several years. While this is great for those who prefer stability, it may not be ideal for homeowners who plan to sell or move within a few years. Early repayment penalties or fees can also make it costly to break the mortgage term early.

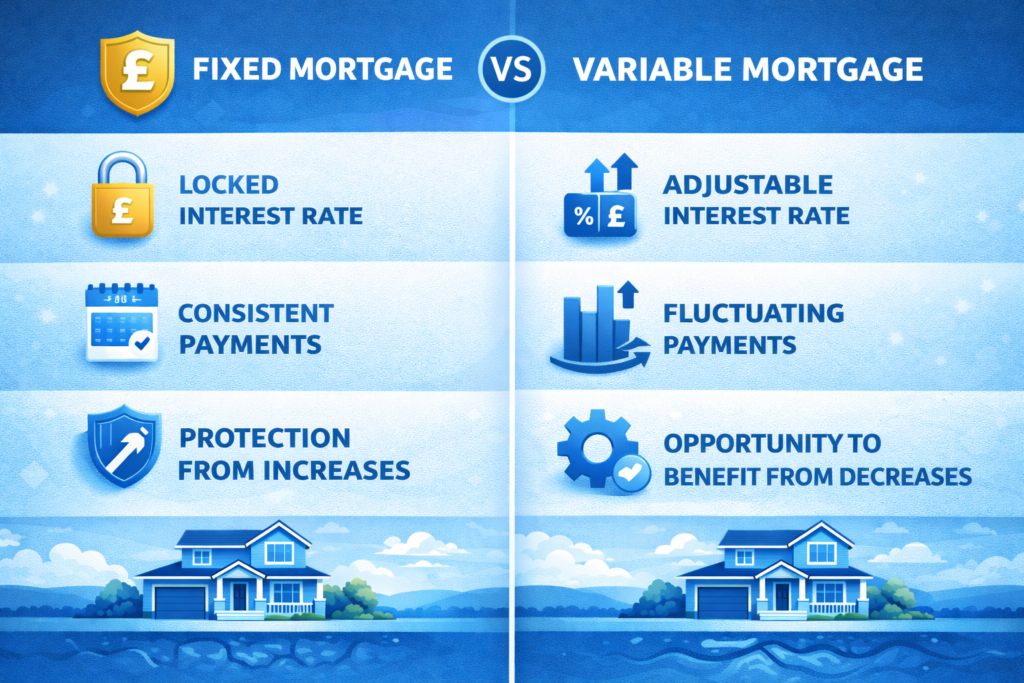

Fixed Mortgage vs Variable Mortgage: Which Is Better for You?

Choosing between a fixed and a variable mortgage depends on your financial goals and preferences. Here’s a quick comparison to help you understand the key differences:

| Feature | Fixed Mortgage | Variable Mortgage |

| Interest Rate | Stays the same for a fixed period. | Can change, often based on market conditions. |

| Monthly Payment | Consistent throughout the term. | Varies depending on interest rates. |

| Risk | Lower risk due to predictable payments. | Higher risk if interest rates rise. |

| Flexibility | Less flexible, especially if rates drop. | More flexibility to take advantage of lower rates. |

| Best For | Those who prefer stability and predictability. | Those who can tolerate fluctuations for lower rates. |

| Suitability | Ideal for long-term homeownership. | Good for short-term or adaptable homeowners. |

How to Apply for a Fixed Mortgage in the UK

Applying for a fixed mortgage in the UK involves a series of steps that will guide you through the process. Here’s what you need to do to secure your mortgage:

Understand What a Fixed Mortgage Is

Before you apply, it’s important to fully understand what a fixed mortgage is and how it works. This step ensures you’re making an informed decision that fits your financial goals.

Check if You Are Likely to Qualify

Eligibility is key in any mortgage application. Lenders will check your credit score, income, and overall financial situation. Ensure you meet the necessary criteria to avoid delays.

Work Out Your Budget

Decide how much you can afford to borrow and whether you’ll be able to handle the monthly payments without financial strain. This helps in selecting the right mortgage deal for your circumstances.

Get Your Documents Ready

Prepare necessary documents like proof of income, bank statements, and identification. Having everything ready will speed up the application process.

Decide: Broker or Direct to a Bank

You can either approach a mortgage broker, who will help you find the best deals, or go directly to a bank. Weigh the pros and cons of both options.

Get an Agreement/Decision in Principle

Request an agreement in principle from your chosen lender. This shows how much you may be able to borrow, based on initial checks.

Find a Property and Make an Offer

Once you have an agreement, you can begin property hunting. When you find the right home, you can make an offer, and the mortgage application process begins.

Choose Your Fixed-Rate Deal

Select the fixed-rate deal that best matches your needs, considering factors like the length of the term and the interest rate.

Submit the Full Mortgage Application

Once your offer on the property is accepted, submit the full mortgage application to your lender for approval.

Property Valuation and Underwriting

The lender will arrange for a property valuation to ensure the property is worth the loan amount. Underwriting will confirm the loan’s terms.

Receive the Mortgage Offer

Once everything is approved, you’ll receive your mortgage offer, and the transaction will move forward.

Common Mistakes to Avoid When Taking Out a Fixed Mortgage

When securing a fixed mortgage, avoiding common mistakes can help you save money and avoid unnecessary stress. Here’s what you need to watch out for:

1. Only Looking at the Monthly Payment

It’s tempting to focus solely on the monthly payment, but you should also consider the overall cost of the mortgage, including any fees or early repayment charges.

2. Not Comparing Different Lenders

Each lender offers different rates and terms. Failing to shop around can result in a less favorable deal. Always compare offers from multiple sources.

3. Ignoring Fees and Extra Charges

Don’t overlook the small print! Many fixed-rate mortgages come with setup fees, valuation charges, or early exit fees. Ensure you’re aware of these costs before signing.

4. Choosing the Wrong Fixed Period

Selecting the wrong term for your fixed mortgage can lead to problems down the road. If you plan on moving soon, a shorter term may be better, while a longer term suits those staying in one home for a while.

5. Borrowing More Than You Can Comfortably Pay

It’s easy to get carried away with borrowing too much, especially if you’re approved for a larger loan. Make sure the repayments fit comfortably within your budget.

6. Not Checking Your Credit First

Your credit score plays a major role in your mortgage approval and interest rate. It’s important to check your credit before applying so you can address any issues in advance.

7. Skipping the Fine Print

Always read the full mortgage agreement carefully. Pay attention to the terms and conditions, especially any clauses regarding penalties or fees for early repayment.

8. Forgetting About Life Changes

Life circumstances change, and it’s essential to factor in any potential changes, such as a new job, additional dependents, or moving in the near future.

9. Not Planning for the End of the Fixed Term

When your fixed term ends, your mortgage may revert to a standard variable rate. Make sure you plan for this and know what your options are when the term is up.

10. Not Asking for Professional Advice

Consulting a mortgage advisor can save you time and money. Professionals can guide you through the process and help you make the best decision for your financial situation.

What Happens After Your Fixed Term Ends?

When your fixed term ends, your mortgage will usually revert to your lender’s standard variable rate (SVR), which may be higher. To avoid this, you can remortgage to another fixed-rate deal or negotiate with your lender for a new fixed rate.

What Happens When You Miss a Payment on a Fixed Mortgage in the UK?

Missing a payment on a fixed mortgage can lead to late fees, damage your credit score, and, in extreme cases, lead to foreclosure. It’s important to contact your lender immediately if you’re having trouble making payments.

The Future of Fixed Mortgages in the UK: Trends to Watch

The future of fixed mortgages in the UK may involve longer fixed terms and more flexible options. As interest rates fluctuate, lenders may introduce new products to give borrowers more control over their payments.

How to Refinance a Fixed Mortgage in the UK

Refinancing your fixed mortgage can provide financial relief or a better deal. Here’s how to go about it:

1. Decide Why You Want to Refinance

Refinancing can help you secure a lower interest rate or adjust your loan term. Be clear about your goals before proceeding.

2. Check Your Current Mortgage Deal

Review your current mortgage to understand your existing terms, including interest rates and fees. This will help you compare it to new refinancing options.

3. Check Your Credit Score and Finances

Ensure that your credit score is healthy, as this will affect the refinancing options available to you. Also, assess your financial situation to confirm you’re in a position to refinance.

4. Work Out Your Loan-to-Value (LTV)

Your LTV ratio is an important factor in securing refinancing. It determines how much equity you have in your property compared to your mortgage balance.

5. Decide: Same Lender or New Lender

You may choose to refinance with your existing lender or look for a better deal elsewhere. Evaluate both options carefully based on fees, rates, and terms.

6. Compare Deals and Costs

Before committing, compare refinancing deals from different lenders. Look at interest rates, fees, and the total cost of the loan to ensure it’s the best option for you.

Frequently Asked Questions (FAQ)

What is the typical interest rate for a fixed mortgage in the UK?

The typical interest rate for a fixed mortgage in the UK varies depending on your lender, credit score, and the length of the term. Rates usually range from 2% to 4% for a 2-5 year fixed period.

What is the current fixed mortgage rate in the UK?

As of the latest market data, the average fixed mortgage rate in the UK is around 2.5% to 3.5% for a 2-year fixed mortgage.

Can I pay off my fixed mortgage early without penalties?

Paying off your fixed mortgage early may incur early repayment charges (ERCs). These penalties depend on the terms of your mortgage agreement.

How long should my fixed mortgage term be?

The length of your fixed mortgage term depends on your financial goals and how long you plan to stay in the property. Common terms range from 2 to 10 years.

What is better, a 3 or 5-year fixed mortgage rate?

A 5-year fixed mortgage rate offers more stability and protection against rate rises compared to a 3-year fixed mortgage. However, it may come with a higher interest rate.

What happens if interest rates fall after I lock in my fixed mortgage?

If interest rates fall after you’ve locked in a fixed rate, you won’t benefit from the lower rates unless you refinance or remortgage at a later time.

Can I switch to a variable mortgage after my fixed term ends?

Yes, once your fixed term ends, you can switch to a variable mortgage. This option allows you to benefit from lower rates if market conditions change.

Is a fixed mortgage better for first-time buyers?

A fixed mortgage is often a good choice for first-time buyers, as it offers predictable payments and stability, making it easier to plan for the future.

How do I know if a fixed mortgage is the right option for me?

A fixed mortgage is a good option if you value stability and want predictable payments. It’s ideal if you plan to stay in your home long-term.

What are the fees associated with fixed mortgages?

Fixed mortgages may involve arrangement fees, early repayment charges, and valuation fees. Always check the full cost of the mortgage before committing.

Can I remortgage before my fixed term ends?

You can remortgage before the end of your fixed term, but you may face early repayment charges. It’s best to consult with a mortgage advisor to determine if this is the right option for you.

Are there fixed mortgage options for buy-to-let investors?

Yes, there are fixed mortgage options available for buy-to-let investors, offering stable payments and predictable costs for property investors.

- Tags:

- buying a house in the UK

- fixed mortgage advice

- fixed mortgage benefits

- fixed mortgage UK

- fixed rate mortgage

- home loan UK +

- mortgage application UK

- mortgage comparison

- mortgage for first-time buyers

- mortgage rates

- mortgage stability

- mortgage types

- remortgaging UK

- UK home loan guide

- UK mortgage options